Personal injury settlements typically range from $20,000 to $75,000 for moderate injury cases, with severe injuries often exceeding $100,000 and catastrophic cases reaching millions. Understanding how much your personal injury case is worth and how insurance companies calculate these amounts can mean the difference between accepting a lowball offer of $15,000 or fighting for a fair settlement of $60,000 or more.

Try our free personal injury settlement calculator.

Table of Contents

- The Reality of Personal Injury Settlement Amounts

- The Settlement Calculation Formula Attorneys Use

- Medical Expenses: The Foundation of Your Settlement

- Lost Wages and Earning Capacity

- Pain and Suffering Multiplier Explained

- Factors That Increase Settlement Values

- Factors That Decrease Settlement Values

- State-by-State Settlement Variations

- Timeline for Receiving Settlement Money

- Why Hiring a Lawyer Triples Average Settlements

- Frequently Asked Questions About Settlement Amounts

- Taking Action: Maximize Your Settlement Value Today

When determining how much your personal injury case is worth, insurance companies use complex formulas they don’t want you to understand.

How Much Is My Personal Injury Case Worth? The Reality

Most personal injury victims receive their first settlement offer within 30-60 days after filing a claim, and that initial offer is almost always significantly below the case’s true value. Insurance companies count on injured victims not understanding the settlement calculation formula, which is why the average unrepresented claimant receives just $17,500, while those with attorneys average $52,500 for similar injuries.

The vast majority of personal injury cases—approximately 95%—settle before trial, with settlements typically falling into these categories:

- Minor soft tissue injuries: $5,000 to $25,000

- Moderate injuries requiring surgery: $30,000 to $85,000

- Severe injuries with permanent effects: $75,000 to $250,000

- Catastrophic injuries: $250,000 to several million

These ranges vary dramatically based on liability clarity, insurance coverage limits, and state laws. A broken arm from a slip-and-fall might settle for $45,000 in California but only $25,000 in Texas due to different legal environments and jury verdict trends.

To determine how much your personal injury case is worth, attorneys and insurance adjusters use specific formulas that most victims never learn about. Understanding these calculations is essential for evaluating any settlement offer.

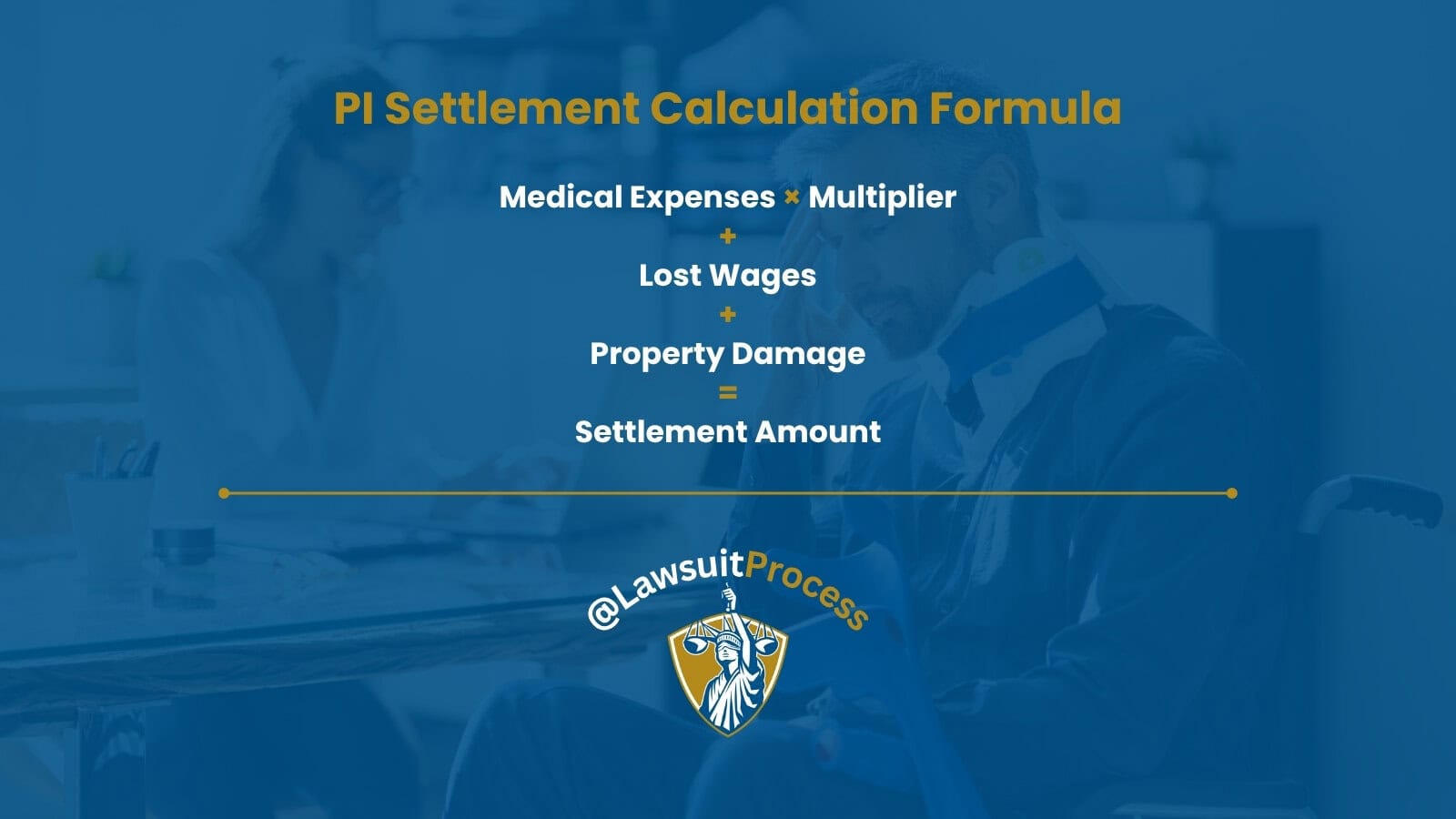

How Attorneys Calculate What Your Personal Injury Case Is Worth

Professional attorneys and insurance adjusters use a specific formula to calculate personal injury settlements, though they rarely share this information with claimants. The basic formula multiplies special damages (economic losses) by a severity multiplier, then adds additional compensation for unique factors.

Base Calculation Method

Total Settlement = (Medical Expenses × Multiplier) + Lost Wages + Property Damage + Additional Damages

The multiplier typically ranges from 2 to 5 for most cases:

- Multiplier of 2-3: Minor injuries with full recovery expected within 3-6 months

- Multiplier of 3-4: Moderate injuries requiring surgery or extended treatment

- Multiplier of 4-5: Severe injuries with permanent effects or disability

- Multiplier of 5+: Catastrophic injuries, wrongful death, or gross negligence

Real-World Calculation Example

Consider a rear-end collision causing a herniated disc requiring surgery:

- Medical expenses: $42,000

- Lost wages (3 months): $15,000

- Property damage: $8,500

- Pain and suffering multiplier: 3.5

Settlement calculation: ($42,000 × 3.5) + $15,000 + $8,500 = $170,500

Insurance companies initially offered this actual client $35,000, claiming the herniated disc was pre-existing. After attorney involvement and proper documentation, the case settled for $165,000—nearly five times the initial offer.

Calculate Your Case Value: Now that you understand the formula, use our free personal injury settlement calculator to estimate your settlement in 60 seconds.

Medical Expenses: The Foundation of Your Settlement

Medical expenses are the primary factor in determining how much your personal injury case is worth, but not all medical costs carry equal weight. Insurance companies scrutinize every medical bill, often challenging treatments they deem “excessive” or “unnecessary.”

High-value medical expenses that strengthen settlements:

- Emergency room visits: $3,000-$15,000 per visit

- Surgical procedures: $15,000-$75,000

- MRI and CT scans: $1,500-$5,000 each

- Physical therapy: $150-$350 per session

- Specialist consultations: $400-$800 per visit

Frequently challenged expenses that may reduce settlement value:

- Chiropractic care exceeding 3 months: Often capped at $5,000

- Alternative treatments (acupuncture, massage): Limited to $2,500

- Excessive diagnostic testing: Adjusters flag more than 3 MRIs

- Treatment gaps exceeding 30 days: Can reduce claims by 20-40%

Future medical expenses require expert testimony but can dramatically increase settlements. A 35-year-old requiring lifetime pain management might add $200,000 to $500,000 to their settlement based on projected costs of $5,000 to $10,000 annually.

Lost Wages and Earning Capacity

Lost wages include both past and future income losses. Past lost wages are straightforward—if you earned $5,000 monthly and missed 4 months of work, that’s $20,000 in economic damages. However, future lost wages and diminished earning capacity can multiply settlements significantly.

A construction worker earning $65,000 annually who can no longer perform physical labor might claim diminished earning capacity of $25,000 yearly until retirement. Over 20 years, that’s $500,000 in future losses, though settlements typically discount this to present value, around $350,000.

Self-employed individuals face unique challenges proving lost income. Tax returns showing $45,000 annual profit carry more weight than claiming $100,000 in undocumented cash earnings. Detailed profit-and-loss statements, contracts, and customer communications strengthen these claims.

Pain and Suffering Multiplier Explained

Pain and suffering compensation—the multiplier applied to medical expenses—varies based on injury severity, recovery duration, and life impact. Insurance companies use software programs like Colossus that assign point values to different factors:

Factors increasing the multiplier:

- Permanent scarring or disfigurement: Adds 0.5-1.0 to multiplier

- Emotional trauma requiring therapy: Adds 0.3-0.7 to multiplier

- Loss of life enjoyment (can’t play sports, hobbies): Adds 0.3-0.5

- Impact on marital relations: Adds 0.2-0.4 to multiplier

- Chronic pain lasting over 6 months: Adds 0.5-1.0 to multiplier

Documentation that maximizes pain and suffering:

- Pain journals detailing daily limitations

- Prescription records for pain medication

- Mental health treatment records showing anxiety, depression, PTSD

- Witness statements about personality changes

- Photos/videos showing inability to perform previous activities

Factors That Increase Settlement Values

Several factors can push settlements well above average ranges. Understanding these elements helps maximize your claim’s value.

Permanent Injury or Disability

Permanent injuries command premium settlements. A facial scar might add $25,000 to $100,000 depending on visibility and victim’s age. Permanent disability affecting work capacity can add hundreds of thousands. A 30-year-old teacher suffering traumatic brain injury affecting cognitive function might receive $2-3 million versus $75,000 for temporary concussion symptoms.

Clear Liability

When fault is undisputed, settlements increase 30-50%. Drunk driving cases, commercial vehicle accidents with driver violations, and premises liability with building code violations typically settle for maximum insurance policy limits. A drunk driver causing $50,000 in damages often triggers $100,000 minimum settlements due to punitive damage potential.

Multiple Defendants

Cases involving multiple responsible parties increase settlement potential. A trucking accident might involve the driver, trucking company, cargo loader, and maintenance provider. Each defendant’s insurance represents additional recovery sources, turning a $100,000 case into a $400,000 settlement.

High Insurance Limits

Commercial policies and umbrella coverage enable larger settlements. While minimum state coverage might be $25,000, commercial trucks carry $1 million minimum, and many businesses have $5-10 million umbrella policies. Identical injuries can yield vastly different settlements based purely on available coverage.

Sympathetic Plaintiff

Certain plaintiffs receive higher settlements: children, elderly victims, pregnant women, and community heroes (teachers, nurses, firefighters) often receive 20-40% above average. A pregnant woman suffering placental abruption from an accident might receive $150,000 for injuries that would typically warrant $75,000.

Factors That Decrease Settlement Values

Understanding what reduces settlement values helps avoid costly mistakes during your claim.

Pre-existing Conditions

Insurance companies aggressively investigate medical histories, seeking pre-existing conditions to minimize payouts. That decade-old workers’ compensation claim for back pain becomes ammunition to argue your herniated disc existed before the accident. However, aggravation of pre-existing conditions is compensable—the key is proving the accident worsened your condition.

Typical reductions for pre-existing conditions:

- Prior treatment for same body part: 20-40% reduction

- Degenerative conditions visible on imaging: 15-30% reduction

- Previous similar injury claims: 25-50% reduction

- Chronic conditions (arthritis, fibromyalgia): 10-25% reduction

Shared Fault/Comparative Negligence

Most states reduce settlements based on your fault percentage. If you’re 20% at fault for speeding when hit by a red-light runner, your $100,000 settlement becomes $80,000. Some states bar recovery entirely if you’re 50% or more at fault.

Common fault allegations that reduce settlements:

- Distracted driving (phone use): 10-30% fault assigned

- Speeding: 5-20% fault assigned

- Failure to avoid accident: 10-25% fault assigned

- Not wearing seatbelt: 5-15% reduction (state-dependent)

- Jaywalking in pedestrian accidents: 20-50% fault assigned

Treatment Gaps and Non-compliance

Missing medical appointments or delaying treatment devastates settlement values. A 30-day treatment gap might reduce settlements by 25%, while 60-day gaps can cut values in half. Insurance companies argue gaps indicate either recovery or exaggeration.

Social Media Evidence

Insurance investigators routinely monitor claimants’ social media. That Facebook photo at a concert during your “debilitating back pain” period can eliminate pain and suffering compensation entirely. Private settings don’t guarantee protection—friends and family sometimes provide information to investigators.

State-by-State Settlement Variations

How much your personal injury case is worth varies dramatically by state due to different laws, jury verdict trends, and economic factors.

California: The High-Value State

California consistently yields higher settlements due to plaintiff-friendly laws and high jury verdicts. Average settlements run 30-40% higher than national averages:

- Whiplash settlements: $15,000-$35,000 (versus $8,000-$20,000 nationally)

- Broken bones: $75,000-$150,000 (versus $45,000-$85,000 nationally)

- Herniated discs: $125,000-$300,000 (versus $75,000-$175,000 nationally)

California’s pure comparative negligence rule allows recovery even if you’re 99% at fault, though reduced proportionally. No damage caps except medical malpractice ($250,000 for pain and suffering) increase settlement potential.

Texas: The Tort Reform State

Texas tort reform significantly impacts settlements. Damage caps and modified comparative negligence (barring recovery if 51% at fault) reduce average settlements:

- Whiplash settlements: $6,000-$18,000

- Broken bones: $35,000-$75,000

- Herniated discs: $60,000-$140,000

Texas’s controversial “paid or incurred” rule limits medical expense recovery to amounts actually paid, not billed amounts. If your $50,000 hospital bill was reduced to $15,000 by health insurance, you can only claim $15,000.

New York: The No-Fault Complexity

New York’s no-fault insurance system complicates settlements. Minor injuries are handled through Personal Injury Protection (PIP) coverage without accessing pain and suffering compensation. Only “serious injuries” as legally defined qualify for liability claims:

- Whiplash settlements (if serious): $20,000-$45,000

- Broken bones: $60,000-$125,000

- Herniated discs: $100,000-$250,000

New York’s pure comparative negligence and high cost of living drive settlements above national averages for serious injuries, while minor injuries receive minimal compensation.

Florida: The Insurance Crisis State

Florida’s insurance crisis and recent tort reforms create unpredictable settlement environments:

- Whiplash settlements: $8,000-$25,000

- Broken bones: $40,000-$85,000

- Herniated discs: $75,000-$175,000

Florida eliminated no-fault insurance in 2023, potentially increasing settlement access but also raising uninsured motorist concerns. Many drivers carry state minimums ($10,000), severely limiting recovery regardless of injury severity.

Timeline for Receiving Settlement Money

Understanding settlement timelines helps manage expectations and financial planning.

Typical Settlement Timeline

Months 1-3: Initial Phase

- Accident occurs, medical treatment begins

- Insurance claim filed, initial investigation

- First settlement offer (usually lowball): 30-60 days post-accident

- Offers typically 20-40% of fair value

Months 3-6: Active Negotiation

- Medical treatment continues or concludes

- Demand letter sent with full documentation

- Multiple rounds of offers and counteroffers

- Most cases settle in this window if represented by attorneys

Months 6-12: Escalation Phase

- Filing lawsuit if negotiations stall

- Discovery process begins

- Depositions scheduled

- Mediation attempted (85% of cases settle here)

Months 12-18: Trial Preparation

- Expert witnesses retained

- Trial date set

- Last-minute settlement negotiations

- Only 5% actually go to trial

Factors Affecting Timeline

Faster settlements (3-6 months):

- Clear liability with adequate insurance

- Completed medical treatment

- Organized documentation

- Reasonable settlement expectations

- Attorney representation from day one

Slower settlements (12-18+ months):

- Disputed liability

- Ongoing medical treatment

- Multiple parties involved

- High-value claims requiring litigation

- Insurance company bad faith tactics

Once settled, payment typically arrives within 2-6 weeks. The process involves signing releases, insurance company processing, attorney fee deduction, and lien resolution (medical providers, health insurance).

Why Hiring a Lawyer Triples Average Settlements

The question of how much your personal injury case is worth often depends on whether you have legal representation. Statistics consistently show attorney representation triples average settlements. Insurance industry studies confirm represented claimants receive 3.5 times more than unrepresented victims, even after attorney fees.

The $17,500 vs. $52,500 Reality

Unrepresented claimants average $17,500 for moderate injury claims, while attorney-represented clients average $52,500 for identical injuries. After typical 33% contingency fees, represented clients net $35,000—still double the unrepresented amount.

How Attorneys Maximize Values

Immediate preservation of evidence: Attorneys send spoliation letters preventing evidence destruction, secure surveillance footage, and document scene conditions before they change.

Medical treatment coordination: Attorneys refer to doctors who properly document injuries for legal purposes, ensuring continuous treatment without gaps, and securing future medical cost opinions.

Aggressive investigation: Private investigators, accident reconstructionists, and biomechanical experts strengthen liability and damage claims.

Insurance company psychology: Adjusters offer more knowing attorneys will file suit if lowballed. Litigation costs $50,000-$100,000 for insurers, motivating fair settlements.

Policy limit discovery: Attorneys uncover all available insurance, including umbrella policies, commercial coverage, and uninsured motorist benefits often missed by claimants.

Frequently Asked Questions About Settlement Amounts

1. How much is my personal injury case worth for a rear-end accident?

Rear-end collision settlements average $25,000 to $65,000 for moderate injuries with clear liability. Minor whiplash cases settle for $8,000 to $20,000, while herniated discs from rear-end impacts average $75,000 to $150,000. High-speed impacts with commercial vehicles often exceed $200,000.

2. How much is my personal injury case worth if I have a herniated disc?

Herniated disc settlements range from $60,000 to $300,000 depending on treatment required. Conservative treatment (injections, therapy) typically yields $60,000 to $100,000. Single-level fusion surgery cases average $150,000 to $250,000. Multi-level fusions can exceed $500,000 with future medical needs.

3. Do I have to pay taxes on my personal injury settlement?

Physical injury settlements are generally tax-free under IRC Section 104(a)(2). However, punitive damages and interest are taxable. Lost wage portions might be taxable depending on claim structure. Emotional distress damages without physical injury are taxable. Consult a tax professional for specific guidance.

4. How much will I get after attorney fees?

Most personal injury attorneys charge 33% for pre-litigation settlements and 40% for cases requiring lawsuit filing. From a $100,000 settlement with 33% contingency, you’d receive $67,000 after attorney fees. Additional costs (medical records, experts) typically range $2,000 to $10,000, further reducing net recovery.

5. What if the at-fault driver has minimum insurance?

If damages exceed policy limits, options include: your uninsured/underinsured motorist coverage (often matching liability limits), personal assets of at-fault driver (rarely collectible), additional responsible parties (employer, bar that overserved), or bad faith claims against insurance company for refusing reasonable settlements.

6. How long do I have to file a claim?

Personal injury statute of limitations varies by state: 2 years in most states including California and Texas, 3 years in New York, 2 years in Florida (recently reduced from 4 years). Claims against government entities often require notice within 6 months. Never wait—evidence disappears and witnesses forget.

7. Should I accept the first settlement offer?

First offers average 20-40% of fair value. Insurance companies expect negotiation and build lowball offers into their process. Accepting first offers leaves significant money on the table. Even without attorneys, counteroffering typically doubles initial offers. One study showed 85% of claimants who rejected first offers received at least 40% more.

8. How much is my case worth if I was partially at fault?

Most states allow recovery even with partial fault, reduced by your fault percentage. Pure comparative negligence states (California, New York) allow recovery even if you’re 99% at fault. Modified comparative negligence states (Texas, Florida) bar recovery if you’re 51% at fault. Document evidence supporting the other party’s greater fault.

9. Can I reopen my settlement if my injuries worsen?

Generally no—settlements include releases barring future claims. Exceptions exist for fraud, minors’ settlements requiring court approval, or reserved rights for specific future conditions. This finality is why completing treatment before settling is crucial. Rushing settlements to pay bills often costs tens of thousands long-term.

10. How much does a demand letter increase settlement offers?

Professional demand letters typically double or triple initial offers. A well-documented demand showing $75,000 in damages often converts $15,000 initial offers into $45,000 to $60,000 settlements. Key components include medical record summaries, bill itemizations, lost wage documentation, and liability analysis.

Finding Out How Much Your Personal Injury Case Is Worth

Every day you wait to properly evaluate your personal injury claim costs money. Insurance companies count on delay, hoping evidence disappears, witnesses forget, and financial pressure forces cheap settlements. The difference between accepting a quick $20,000 settlement and fighting for fair compensation of $75,000 or more often comes down to taking immediate action.

Don’t let insurance companies minimize your claim’s value. Getting a free case evaluation from an experienced personal injury attorney costs nothing but could mean the difference between covering your medical bills and securing your financial future. Most attorneys offer free consultations, work on contingency (no fee unless they win), and can typically tell you within minutes whether you’re being offered fair value.

Take action now: Document everything, continue medical treatment, avoid social media posts about your accident, never give recorded statements without legal advice, and most importantly, get your free case evaluation to learn how much your personal injury case is worth before accepting any settlement offer. That 30-minute consultation could be worth $50,000 or more in additional compensation.

Related Resources: